Print Story

X

All projects have benefits and costs. CPEC too has its downsides and it is necessary to identify them and adopt mitigating measures

The China Pakistan Economic Corridor (CPEC) does promise to be a game changer for Pakistan. It is a project of a magnitude that will change the economic geography of the country. An earlier project that changed the economic geography of the country was the Indus Water Works which included the construction of Mangla and Tarbela dams along with thousands of kilometres of canals. Resultantly, two crops a year are now grown where not a blade of grass grew and bustling towns exist in places that were dusty landscapes till the 1970s.

Resultantly, two eastern provinces -- Punjab and Sindh -- stand developed as the metropolitan areas, while the two western provinces -- Balochistan and Khyber Pakhtunkhwa (KP) -- and Gilgit Baltistan have remained peripheral to the national economy. Now CPEC’s western route promises to be a harbinger of change for these regions.

CPEC also holds the potential to change the political geography of the region. Culturally and politically, Pakistan lies on the border of south and west Asia. Two eastern provinces -- Punjab and Sindh -- are firmly part of South Asia. And two western provinces -- Balochistan and Khyber-Pakhtunkhwa -- are more akin to west than to south Asia. There is a Punjab province in Pakistan as well as in India and Punjabi is a language common to both countries. The Baloch population resides in Pakistan as well as in Iran and Farsi (Persian) is widely spoken in Balochistan and is also one of the official languages of the province. Pushtu is a language common to KP and Afghanistan. Close family links exist between Pakhtun families in KP and Afghanistan and between Baloch families in Balochistan and the Sistan Baluchistan province of Iran. Gilgit Baltistan (and Peshawar valley) has had centuries-old linkages with Sinkiang in China and with central Asia.

For geopolitical reasons, all travel and trade connections with Sinkiang and central Asia were severed during the first quarter of the 20th century and remained so till very recently. It was as if the world did not exist to the north/north-west of Gilgit Baltistan and Afghanistan. CPEC promises to unlock many of the doors, hitherto closed, and open up a vast area to the north and north-west.

To the south, Gwadar and Chahbahar are destined, de facto even if not de jure, to emerge as twin ports, complementing each other. Today, Pakistan is largely a south Asian player; post-CPEC, Pakistan is likely to emerge as a central and west Asian power as well. Tentative steps towards the development of Pakistan-Russia relations and Russian and Chinese initiatives for peace in Afghanistan can be seen in this context.

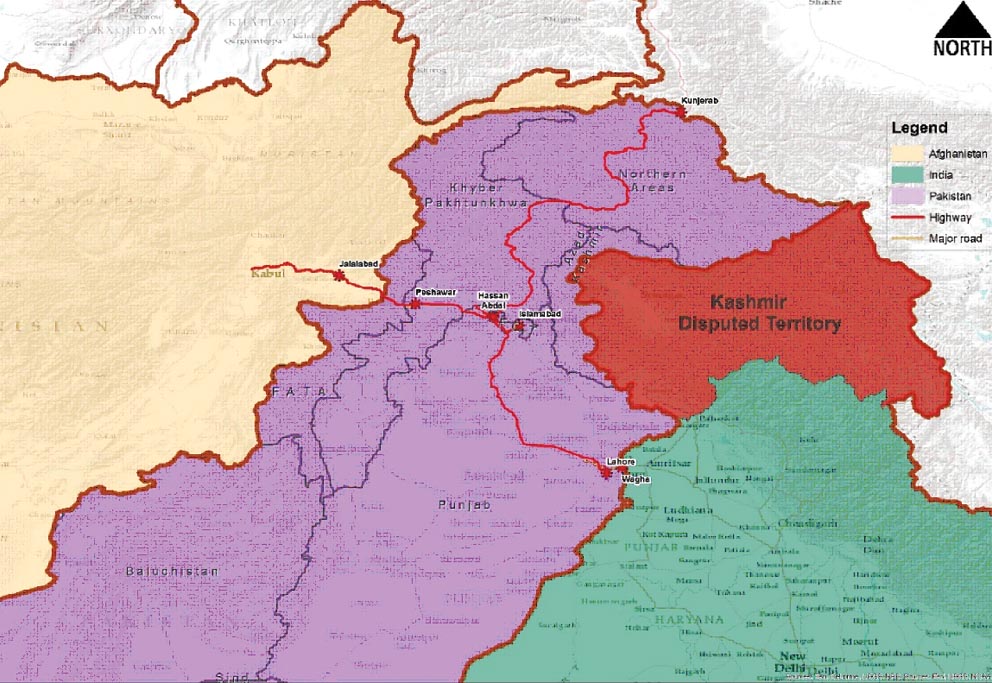

To the east, CPEC is likely to "impose" a de facto loosening of the Pakistan-India gridlock. As Chinese trucks ply 2,000 kilometres between Gwadar and Kashgar, they will inevitably pass Hasan Abdal, which incidentally is a mere 300 kilometres from the Indian border. For China, the 700 kilometre Kashgar-Hasan Abdal-Amritsar route would beckon as yet another shorter and lucrative route to expanding trade with an economically resurgent India -- already exceeding USD 100 billion along the 5,500 kilometre Shanghai-Mumbai sea route.

China is likely to pressure Pakistan for allowing Chinese trucks to proceed to and from India on the Hasan Abdal-Wagah route. It is then likely that Indian trucks are also allowed to use the Amritsar-Hasan Abdal-Kashgar route. And it is then also likely that Indian trucks, allowed into Pakistani territory up to Hasan Abdal on way to Kashgar, are allowed to proceed the balance 450 kilometres from Hasan Abdal to Kabul. While unimaginable at this point of time, given the vast and complicated geopolitical baggage, travel and trade barriers between India, Pakistan and Afghanistan can possibly come down a la Berlin Wall.

Pakistan’s China equation vis-à-vis CPEC appears to be India-centric. What needs to be kept in mind is that China and India, despite their history of armed conflict, border dispute and rivalry for supremacy, are not mortal enemies. China-India trade exceeds 100 billion USD and rising, compared to China-Pakistan trade at a stagnant 12-14 billion USD. China and India are least likely to go to war and any thought that China will go to war on behalf of Pakistan is laughable. China is actively wooing India to persuade it to join One Belt One Road and it is only a matter of time before India does, even if in a limited way. In that event, Pakistan’s strategy of using China to shield itself from India will be in tatters.

Potential risks

All projects have benefits and costs. CPEC too has its downsides and it would be necessary to identify the downsides and adopt mitigating measures. At times, the mitigation of human and social costs are as important as the project itself.

Much, however, depends on how a scheme is designed. As such, the extent to which CPEC will be beneficial to Pakistan will depend on how the component schemes are devised and implemented. Many claims and comments are being made about CPEC. Most, if not all, do not appear to be based on empirical analysis -- on account of the fact that sufficient data or information regarding CPEC is not publicly available.

Here is a set of 12 questions, the answers to which will help form a basis of informed discussion.

Questions 1 and 2 are overarching. Any move -- and one as fundamental as the Gwadar development mega-project -- needs to be studied a priori with respect to its benefits and costs. If CPEC’s overall feasibility in terms of economic, social, environmental, political and military impacts has not been carried out, it would amount to jumping in the sea with blindfolds.

Our national economy

Questions 6, 7, 8 and 9 are crucially relevant to the national economy. Potentially, CPEC can pose three macroeconomic hazards for Pakistan’s economy: to the manufacturing sector, to Balance of Payments stability and to fiscal balance stability.

Impact on manufacturing sector

Pakistan’s manufacturing sector stands in serious danger from two factors unless prior protective measures are adopted. Experience shows that an allegedly large part of goods from the Afghan transit trade, transiting through Karachi port, are off-loaded in Pakistan or makes its way back. These de facto tax free products compete with de jure taxed products manufactured in the country and has caused many industries to shut down altogether. The Gwadar-Kashgar traffic is another name for China transit trade, with a thousand times more value. The impact of even one per cent of the goods in transit leaking into the Pakistan market a la Afghan transit goods can be imagined.

Further, experience again shows that tax exemptions to industries or to regions have only created distortions, without benefitting the economy. With regard to CPEC, the sweeping tax exemptions being awarded to Chinese firms creates a highly damaging non-level and discriminatory playing field against Pakistani firms, with the potential to virtually eliminate the remaining locally owned manufacturing sector in the country.

The argument that tax exemptions are available to all firms located in industrial zones, irrespective of nationality, is flawed. Empirical results shows that such exemptions are used by industries located outside the tax-free zones to set up token facilities in the tax-free zones and claim benefits to boost profits from their operations elsewhere in the country. Gadoon-Amazai is a classic example. That foreign firms will resort to similar tactics cannot be discounted.

Balance of Payments stability

Pakistan’s Balance of Payments has always been in the red, but manageable, despite occasional crisis points. The negative balance is created on account of deficits in the trade as well as services/income balances. Post-2000, however, the income deficit (as part of services balance) has risen sharply to merit attention.

The income deficit phenomenon has arisen on account of privatisation of large service sector enterprises in banking, telecommunications, etc. sectors and inflows of foreign direct investment (FDI) in service sectors -- food, retail trade, etc. All these foreign firms earn their revenues in rupees, but remit their profits in foreign exchange. These firms do not earn any foreign exchange for Pakistan, given that few -- if any -- of them operate in the manufacturing sector and do not have any ‘produce’ to export. Resultantly, there have not been foreign exchange inflows corresponding to foreign exchange outflows.

CPEC-related foreign and foreign-supported investments is largely, if not almost exclusively, in the form of loans and FDI. The former will entail debt servicing and the latter profit remittance to host countries. If corresponding foreign exchange inflows are not ensured -- and this is critically important -- there is likely to be a Balance of Payments crisis of gargantuan proportions and Pakistan’s economic and political sovereignty can be at stake.

Fiscal stability

Security expenditure:

Pakistan’s commitment to CPEC extends to providing maximum security on land and at sea. To this end, it is raising dedicated security units, which will entail rupee costs to be met from the national budget, unless funded autonomously. There can be three or more sources of funding this cost.

Water: The water availability question in Gwadar is serious, but always brushed under the carpet to avoid discussion. A hackneyed answer is that dams will be constructed. However, dams do not produce water, they only store available water. And, in Gwadar and all along the Balochistan coast, rains are the only source of water. And rains are erratic, with drought periods extending to 3 years or more.

The other source of water is the sea -- i.e., desalination. However, desalination is exorbitantly expensive. Here again, providing a permanent subsidy from the budget will lead to an exploding budget deficit; leading to the possibility of hyper-inflation or crippling tax rises. Given the strategic importance of Gwadar and the imperative to develop the port, a water solution is essential and one source is the sea. However, a financing plan needs to be developed, with a permanent built-in cross-subsidy from a Gwadar port-related revenue source. If Pakistan’s cost of providing water to Gwadar is greater than Pakistan’s share in Gwadar Port revenues, CPEC is a losing proposition.

The above are expressions of potential pitfalls. All of them can be coped with, provided they are recognised upfront -- and managed. If not, it is a moot point whether future historians will be writing about CPEC as a game changer or game over!

Questions of relevance to Balochistan

Questions 3, 4, 5, 10, and 11 relate to Balochistan. CPEC is Gwadar and Gwadar is Balochistan. If Balochistan’s share of economic benefits are not substantial, then CPEC is irrelevant to the province. Mention has been made earlier of the three necessary conditions -- connectivity, urban development and human resource development -- without which CPEC will not be a game changer for Balochistan.

Additionally, a meaningful share of Balochistan’s Gwadar port revenues and proportionate share of highway toll revenues, in terms of highway share passing through Balochistan, need to be ensured. A proportionate share, again in terms of highway share passing through Balochistan, needs to be ensured in recruitment of personnel for CPEC security. If not, the security units will be perceived as occupation forces. And finally, there is a danger of a cataclysmic demographic change in Gwadar, with migrant workers from the rest of Pakistan -- and from abroad -- pouring in to fill in emerging jobs. Effective constitutional, legislative and administrative measures need to be taken to ensure that the Baloch do not become a minority, relegated to enclaves, in the port city and adjacent areas.

In this essay, Kaiser Bengali follows up on the interview titled "CPEC is not game-changer, it’s game over", carried on this page on September 3, 2017. With this we open our pages for more contributions on the subject.