Analysis: A pragmatic budget

A 5pc GDP growth target for FY23 is neither advisable nor likely and the IMF programme will be secured, allowing friendly countries to retain support and the government to refinance debt

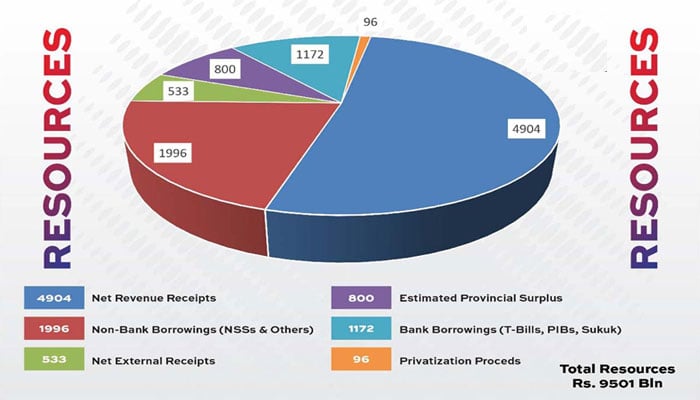

Caught between a rock (IMF) and a hard place (popularity), the commodity supercycle and devaluation came to the government’s rescue to help bridge the tax revenue target through higher import values.

This allowed the FM to limit the impact of additional taxes and find the space to retain some element of growth. However, a 5pc GDP growth target for FY23 is neither advisable nor likely. The IMF programme will be secured, allowing friendly countries to retain support and the government to refinance debt. The dilemma is that inflation, which undermines government’s popularity, will help it meet the tax revenue target and secure the IMF programme.

However, reliance on the commodity supercycle to meet revenue targets is not a sustainable solution and mini-budgets can be expected if it subsides.

Devoid of political will to broaden the tax base, the budget uses the traditional formulae of taxing the taxed through windfall tax on companies and individuals earning over Rs300 million, 3pc higher tax on banks and compression of salary tax slabs. It could have been worse for the formal sector. At least, some direction is visible in taxing immoveable property. Import levies are to be rationalised on 400 lines to promote manufacturing, initial allowance on capital expenditure has been doubled and non-filers will have to pay advance tax at twice the rate hitherto applicable on purchase of 1600cc and larger cars.

To its credit, the government has reversed the retrogressive sales tax on solar equipment and seeds. Also, agricultural equipment will be exempted from import duty. An industrial policy is being developed and SEZs are to be accelerated to promote investment. Promises of prompt refund of taxes and payment of rebates have been made in the past. There is a need to walk the talk. Imports are forecast to decline and exports to rise. However, there are no visible measures in the budget to facilitate this.

Notwithstanding, a 20-year-old crisis of funding a bloated government, losses of state-owned enterprises and mounting debt service charges, the government found space to increase government wages and pensions.

The FM had an unenviable task of making a budget under tough conditions. Whilst business expected reversal of double taxation of intercorporate dividends and restoration of incentive to list companies on the PSX, this will need to wait. Resources need to be deployed on more focused and targeted subsidies to the poor.

The writer is CEO of Pakistan Business Council.

-

Blac Chyna Reveals Her New Approach To Love, Healing After Recent Heartbreak

Blac Chyna Reveals Her New Approach To Love, Healing After Recent Heartbreak -

Royal Family's Approach To Deal With Andrew Finally Revealed

Royal Family's Approach To Deal With Andrew Finally Revealed -

Super Bowl Weekend Deals Blow To 'Melania' Documentary's Box Office

Super Bowl Weekend Deals Blow To 'Melania' Documentary's Box Office -

Meghan Markle Shares Glitzy Clips From Fifteen Percent Pledge Gala

Meghan Markle Shares Glitzy Clips From Fifteen Percent Pledge Gala -

Melissa Jon Hart Explains Rare Reason Behind Not Revisting Old Roles

Melissa Jon Hart Explains Rare Reason Behind Not Revisting Old Roles -

Meghan Markle Eyeing On ‘Queen’ As Ultimate Goal

Meghan Markle Eyeing On ‘Queen’ As Ultimate Goal -

Kate Middleton Insists She Would Never Undermine Queen Camilla

Kate Middleton Insists She Would Never Undermine Queen Camilla -

Japan Elects Takaichi As First Woman Prime Minister After Sweeping Vote

Japan Elects Takaichi As First Woman Prime Minister After Sweeping Vote -

King Charles 'terrified' Andrew's Scandal Will End His Reign

King Charles 'terrified' Andrew's Scandal Will End His Reign -

Winter Olympics 2026: Lindsey Vonn’s Olympic Comeback Ends In Devastating Downhill Crash

Winter Olympics 2026: Lindsey Vonn’s Olympic Comeback Ends In Devastating Downhill Crash -

Adrien Brody Opens Up About His Football Fandom Amid '2026 Super Bowl'

Adrien Brody Opens Up About His Football Fandom Amid '2026 Super Bowl' -

Barbra Streisand's Obsession With Cloning Revealed

Barbra Streisand's Obsession With Cloning Revealed -

What Did Olivia Colman Tell Her Husband About Her Gender?

What Did Olivia Colman Tell Her Husband About Her Gender? -

'We Were Deceived': Noam Chomsky's Wife Regrets Epstein Association

'We Were Deceived': Noam Chomsky's Wife Regrets Epstein Association -

Patriots' WAGs Slam Cardi B Amid Plans For Super Bowl Party: She Is 'attention-seeker'

Patriots' WAGs Slam Cardi B Amid Plans For Super Bowl Party: She Is 'attention-seeker' -

Martha Stewart On Surviving Rigorous Times Amid Upcoming Memoir Release

Martha Stewart On Surviving Rigorous Times Amid Upcoming Memoir Release