$3bn UAE help for Pakistan’s depleting forex reserves

The United Arab Emirates has agreed to provide $3 billion immediate relief to Pakistan that will help boost its shrinking foreign exchange reserves

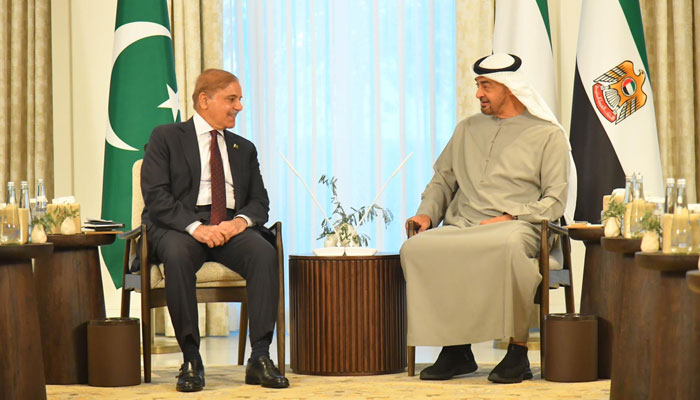

ISLAMABAD/KARACHI: The United Arab Emirates (UAE) has agreed to provide $3 billion immediate relief to Pakistan that will help boost its shrinking foreign exchange reserves.

The relief includes $2 billion existing loan rollover and provision of an additional $1 billion. The decision was taken during a meeting between Prime Minister Shehbaz Sharif and host President, Sheikh Muhammad bin Zayed Al Nahyan.

Shehbaz later met Sheikh Muhammad bin Rashid Al Maktoum, Vice President and Prime Minister of the United Arab Emirates and Ruler of Dubai.

Shehbaz arrived in Abu Dhabi on Thursday on a two-day visit.

Pakistan’s Ambassador to the UAE, Faisal Niaz Tirmizi, shared this development with The News from Abu Dhabi on Thursday evening.

Sheikh Muhammad bin Zayed welcomed Premier Shahbaz Sharif’s visit and wished progress and prosperity for Pakistan. He praised the historical relations between the two nations and the valuable contributions made by the Pakistani community in the Emirates.

The prime minister thanked the UAE president for inviting him to the country. The two leaders discussed the bilateral fraternal relations and explored ways and means to strengthen them, especially in the fields of trade, investment, and energy.

The two leaders also exchanged views on regional and international issues of mutual interest and agreed to deepen the investment cooperation, stimulate partnerships and enable investment integration opportunities between the two countries.

They also expressed satisfaction over the pace of steady progress in bilateral relations and agreed on the importance of enhanced bilateral exchanges and regular dialogue at all levels to further solidify and provide momentum to the relationship.

Shahbaz invited Sheikh Muhammad to a state visit to Pakistan to which he agreed. The dates will be decided through the diplomatic channels. Sheikh Muhammad bin Rashid welcomed the prime minister to Dubai and expressed his best wishes for progress and development of Pakistan under his leadership.

The prime minister thanked Sheikh Muhammad bin Rashid for warmly welcoming him and his delegation and underscored the importance of Pak-UAE relationship.

He also emphasised the exploration of further avenues to deepen the Pakistan-UAE relationship in all fields. Both the leaders discussed ways to enhance the existing bilateral relations at all levels to benefit both nations. They stressed the importance of intensifying and strengthening communication between the private sector of the two countries in order to discuss trade and investment opportunities and turn these into tangible partnerships.

Sheikh Muhammad praised the dedication and hard work of the Pakistani community which significantly contributed towards the development of the UAE.

Prime Minister Shehbaz acclaimed the historical ties between Pakistan and the UAE and reaffirmed his government’s commitment to working closely with the leadership of the UAE to further enhance bilateral cooperation.

The prime minister will also visit Wahat Al Karama to pay homage to the national heroes of the UAE.

UAE Ambassador to Pakistan Hamad Obaid Ibrahim Salem Al-Zaabi is also in the UAE to assist his country’s administration during the visit of Prime Minister Shahbaz Sharif.

In a related development and a huge relief to the PDM government, Pakistan and Saudi Arabia Thursday signed $1 billion worth of oil facility on deferred payment under which the Saudi Fund for Development (SFD) will pay $100 million per month for the purchase of oil for the next 10 months.

“It will continue providing the much-needed breathing space to the struggling economy of Pakistan at a time when the foreign exchange reserves held by the State Bank of Pakistan (SBP) have further depleted and stand at $4.3 billion mainly because of increased foreign debt repayments,” top official sources confirmed while talking to The News.

The sources said the existing oil facility of $1.2 billion had expired in January 2023, as it kick-started in February 2022. The Government of Pakistan made a fresh request and the KSA provided another $1 billion oil facility on deferred payment, which will kick-start from February 2023.

The kingdom also announced augmenting deposits lying in the State Bank of Pakistan to $5 billion from the existing level of $3 billion in order to shore up the dwindling foreign exchange reserves.

In 2019 and 2021, the SFD signed agreements to finance oil derivatives with a value of $4.44 billion.

Meanwhile, the central bank’s foreign exchange reserves fell by $1.2 billion to $4.3 billion as of January 6, leaving the crisis-hit Pakistan with barely three weeks’ worth of import cover.

Reserves are now at their lowest level since February 2014. The reserves held by the State Bank of Pakistan show an alarmingly low import cover. The central bank attributed a decline in reserves to foreign debt repayments.

Last week, the country paid back $600 million to the Emirates NBD Bank and $420 million to the Dubai Islamic Bank.

Pakistan’s total forex reserves fell by $1.2 billion to $10.2 billion, while the commercial banks’ holdings declined by $1 million to $5.8 billion.

“The decline was expected as we made repayments on commercial loans,” said Fahad Rauf, the head of research at Ismail Iqbal Securities.

-

Bridgerton’s Michelle Mao On Facing Backlash As Season Four Antagonist

Bridgerton’s Michelle Mao On Facing Backlash As Season Four Antagonist -

King Charles Gets New ‘secret Weapon’ After Andrew Messes Up

King Charles Gets New ‘secret Weapon’ After Andrew Messes Up -

Shia LaBeouf Makes Bold Claim About Homosexuals In First Interview After Mardi Gras Arrest

Shia LaBeouf Makes Bold Claim About Homosexuals In First Interview After Mardi Gras Arrest -

Princess Beatrice, Eugenie ‘strained’ As They Are ‘not Turning Back’ On Andrew

Princess Beatrice, Eugenie ‘strained’ As They Are ‘not Turning Back’ On Andrew -

Benny Blanco Addresses ‘dirty Feet’ Backlash After Podcast Moment Sparks Online Frenzy

Benny Blanco Addresses ‘dirty Feet’ Backlash After Podcast Moment Sparks Online Frenzy -

Sarah Ferguson Unusual Trait That Confused Royal Expert

Sarah Ferguson Unusual Trait That Confused Royal Expert -

Prince William, Kate Middleton Left Sarah Ferguson Feeling 'worthless'

Prince William, Kate Middleton Left Sarah Ferguson Feeling 'worthless' -

Ben Affleck Focused On 'real Prize,' Stability After Jennifer Garner Speaks About Co Parenting Mechanics

Ben Affleck Focused On 'real Prize,' Stability After Jennifer Garner Speaks About Co Parenting Mechanics -

Luke Grimes Reveals Hilarious Reason His Baby Can't Stop Laughing At Him

Luke Grimes Reveals Hilarious Reason His Baby Can't Stop Laughing At Him -

Why Kate Middleton, Prince William Opt For ‘show Stopping Style’

Why Kate Middleton, Prince William Opt For ‘show Stopping Style’ -

Here's Why Leonardo DiCaprio Will Not Attend This Year's 'Actors Award' Despite Major Nomination

Here's Why Leonardo DiCaprio Will Not Attend This Year's 'Actors Award' Despite Major Nomination -

Ethan Hawke Reflects On Hollywood Success As Fifth Oscar Nomination Arrives

Ethan Hawke Reflects On Hollywood Success As Fifth Oscar Nomination Arrives -

Tom Cruise Feeling Down In The Dumps Post A Series Of Failed Romances: Report

Tom Cruise Feeling Down In The Dumps Post A Series Of Failed Romances: Report -

'The Pitt' Producer Reveals Why He Was Nervous For The New Ep Of Season Two

'The Pitt' Producer Reveals Why He Was Nervous For The New Ep Of Season Two -

Maggie Gyllenhaal Gets Honest About Being Jealous Of Jake Gyllenhaal

Maggie Gyllenhaal Gets Honest About Being Jealous Of Jake Gyllenhaal -

'Bridgerton' Star Luke Thompson Gets Honest About Season Five

'Bridgerton' Star Luke Thompson Gets Honest About Season Five