The technological advancements have changed the dynamics of banking across the globe. With the adoption of new technologies, the scale of disruption in the banking industry is unprecedented across markets, distribution channels and product lines. Significant penetration of digital channels like mobile phones, smart cards, internet, and other technologies are resulting in new innovative business models that deliver financial services at lower prices and with broader customer reach. In Pakistan, with high cell-phone penetration, high internet usage, enabling regulations, and multiple branchless banking operators, digital payments are increasing and will continue to grow.

The technological advancements have changed the dynamics of banking across the globe. With the adoption of new technologies, the scale of disruption in the banking industry is unprecedented across markets, distribution channels and product lines. Significant penetration of digital channels like mobile phones, smart cards, internet, and other technologies are resulting in new innovative business models that deliver financial services at lower prices and with broader customer reach. In Pakistan, with high cell-phone penetration, high internet usage, enabling regulations, and multiple branchless banking operators, digital payments are increasing and will continue to grow.

Mobile and Internet penetration in Pakistan has grown exponentially – more than 84 percent (183 million) of our population uses cellular phones and more than half of them (54 percent+) are 3G/4G connection users. This shows strong penetration within masses for online/ internet access. The government has taken the lead to promote this trend with enabling regulation and products to facilitate the digital shift such as Raast, PayPak, and Roshan Digital Account to name a few.

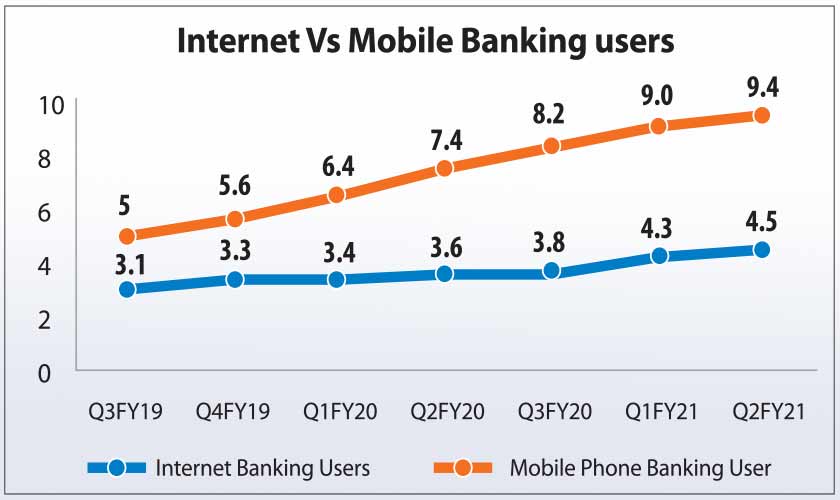

The number of registered Mobile phone banking users reached 9.3 million in Q2 for FY 2021 (October-December ‘20), which is an increase of 5 percent from last quarter. Although, this comprises of only 10 percent of the potential online mobile users. The upward trend has continued with an increase in transactions through internet and mobile banking channels, and with the support of State Bank of Pakistan for digital banking products and initiatives this trend can be expected to continue.

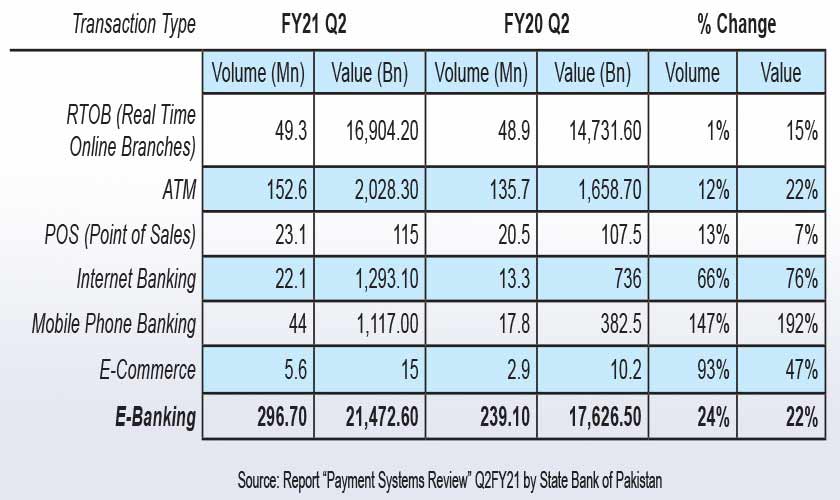

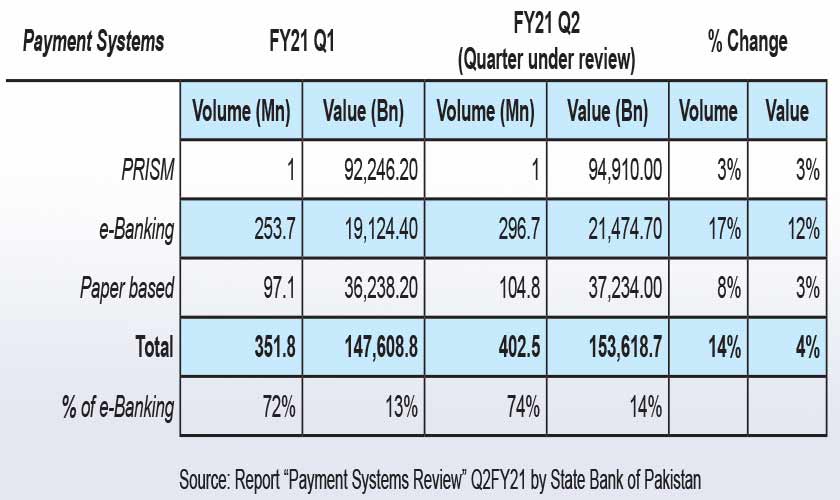

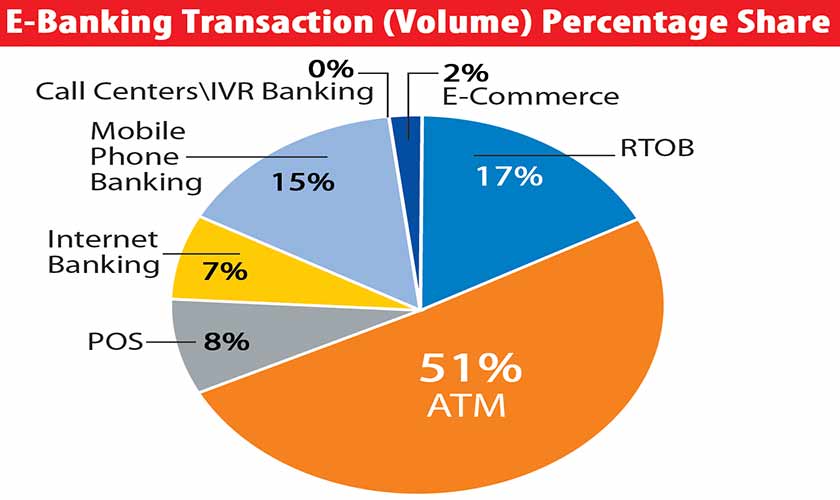

Currently, the share of e-banking channels ie, real time online branches (RTOB), ATMs, e-commerce, internet, mobile phone and call centers/ IVR banking in total transactions processed is 74 percent in terms of volume but only 14 percent in terms of value.

The digital payment transactions in Pakistan have increased significantly due to the impact of measures taken by the SBP that created incentives for customers, the central bank said in a statement. “Growth in digital payment infrastructure as well as emergence of new payment aggregators have also been a contributing factor in this increase. Moreover, it also reflects the changes in consumer preferences for digital transactions amid the Covid-19 situation.”

During the quarter under review, e-banking channels ie RTOBs, ATM, POS, e-commerce, banking through mobile phone, and internet and call centers altogether processed 296.7 million transactions valuing Rs21.4 trillion.

When comparing this quarter with previous quarter, e-banking has increased by 24 percent in volume and 22 percent in value. As on quarter-end, the number of e-commerce merchants registered with banks rose to 2,411 accounting for 11 percent increase. These merchants processed transactions valuing Rs15 billion during the quarter under review.

In order to enhance the usage of digital payments to the next level and create a behavioral shift towards adoption of digital financial services, there is a need to develop a digital payments eco-system along with a range of retail payment services that allows a person to make payments digitally from anywhere at any time which requires both enabling regulation and service offering.

The State Bank of Pakistan (SBP) has recently announced a proposed digital bank regulatory framework offering detailed guidelines for licensing, and supplementary regulations for digital banks. It sets out different types of digital bank licenses including both retail and full bank license, constitution models, minimum eligibility criteria and key competencies.

This indigenous regulatory framework is designed to enable the industry to exploit the market demand and opportunities without compromising the safety and soundness of the financial system. Moreover, it also provides for investor-friendly, first-of-its-kind, flexible requirements in Pakistan. This is in line with the SBP commitment towards effective and widening penetration of banking

The overall changes in the licensing regime is surely expected to create opportunities for both incumbents with existing banks set to expand upon their digital channels as well as promote new entrants. Like in other emerging markets digital banking in Pakistan is primed for growth; however, it is critical to understand the role that the licensing regime can play in contributing towards the success of this sector. Generally, when we study major similar markets, digital banks operating under more stringent regulations have seen relatively limited growth.

Pakistan presents a unique market for growth in digital payments and finance. It is an emerging economy projected to be among the fastest growing in the coming years with a strong projected growth rate after recovery from the pandemic. Despite the economy having gone through a difficult period, with a significant balance of payments issue and a currency under pressure, the intrinsic drivers suggest tailwinds for growth.

Recent surveys exploring Pakistan’s potential’, gathered perspective of individuals with diverse age demographics, income brackets, employment/business backgrounds, across different geographies to analyse how they like to interact with their banks, use branches or alternate channels and how receptive they are to new age banking.

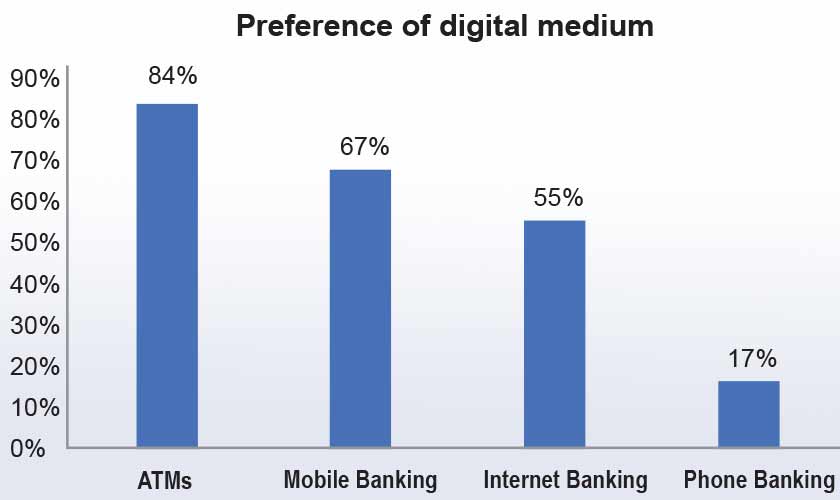

One such survey found growing usage of alternate channels. Eight four percent respondents said they preferred to use ATMs, 67 percent mobile banking, 55 percent internet banking and just 17 percent use phone banking.

It was revealed that 86 percent individuals use mobile banking for fund transfer and 85 percent for account balances, while 75 percent used this medium for bill payments and only 17 percent for location-based discount.

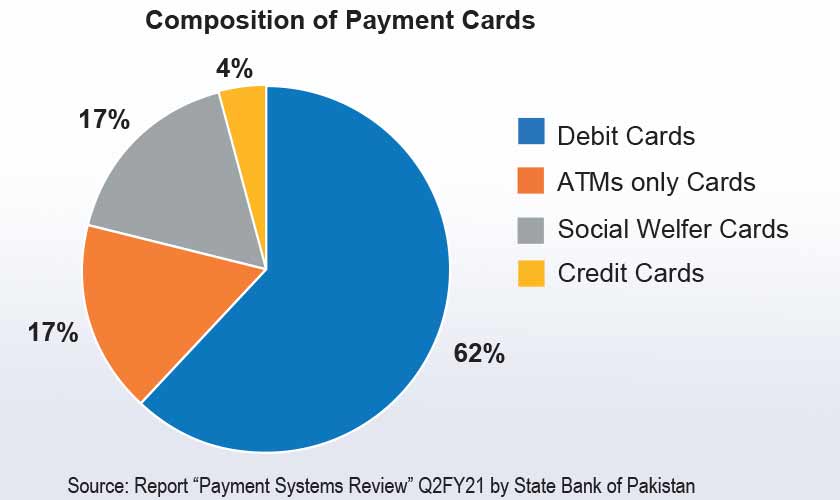

The survey results also found a higher tendency of payments through cards — debit and credit. Around 90 percent respondents said they would like to use cards.

Card-based transactions on e-commerce portals also increased substantially, with e-commerce merchants processing 5.6 million transactions through payment cards amounting to Rs15 billion in the second quarter of FY21 compared to 3.9 million valuing at Rs11.9 billion in the first quarter. This reflects the overall potential for growth of E commerce platforms with increasing penetration of digital banks and payments platforms. Pakistan also has the fifth largest youth population in the world in absolute terms, with roughly half the population under the age of 25 and this means that consumer spending will be driven by the expanding workforce and middle class. Pakistan's e-commerce market size posted a growth of over 35 percent in the first quarter of the fiscal year 2021 to Rs96 billion compared to Rs71 billion over the corresponding period of last year. This growth reflects the untapped potential and presents a huge opportunity in a country which with only 21 percent of the population being banked or using any non-cash-based payment options. Cash still dominates Pakistan's economy, with most wages paid in paper money and merchants largely unable to accept digital payments. Only 21 percent of adults have a transaction account and of these only seven percent are women.

Despite the overall potential the biggest challenge faced by digital banking and payment service operators has been the variety of business and operating models with digital access / delivery channels for conventional banks, payment service operators or micro finance institutions with focus towards offering digital options for micro payments and the need and potential for creating digital only banks as per the draft of the guidelines issued by the SBP.

Whereas there may not be an appropriate fit for all models for a digital bank, success of any business proposition for a digital bank must be based upon its independence from the conventional banking model.

Critical aspects of such a model must be based upon:

• A digital front end to acquire customers including a sales and service model structured with little or no paper documents and without physical interface

• Software / cloud-based back-end operating system with the appropriate digital and technical safeguards expected of any core banking platform

The success of a digital bank will be based upon it being run as what it actually is, that is a technology company, and not a conventional bank therefore should be devoid of complex hierarchal structure and focused towards continued development of systems and products. The success would only be based upon their ability to offer better reach, better customer propositions and more importantly a much more differentiated customer value proposition.

Typical or conventional commercial banks have certainly had an overall advantage in terms of their reach, physical access through customer access channels and branch network however this advantage is fast eroding against real time and measurable turnaround times on key customer needs and requirements.

The value proposition for customers would not only offer an easy to access seamless customer interface but more importantly a simplified online acquisition process for fast customer online request processing such as in principle retail loan approvals for card / autos financing, etc.

The effective digital bank proposition would be towards rapid deployment of higher margin and more profitable banking products through digital penetration and reach to its potential online customers with products such as micro loans, remittances and third-party offerings such as insurance. Success of such models can only be effective when it utilises third party data including tax, utilities, etc to determine payment and spending patterns.

A high degree of adaptability and scalability is necessary to target high volume and low value customers and typically focused towards small and micro customers to tap the potentially attractive unbanked market. Customer onboarding and acquisition should be structured through using various databases effectively such as data from telecoms to identify potential target customers and using social media channels effectively.

The current environment in Pakistan will be a tough market for any new digital only bank to compete. There is no business activity or sector best suited to such digital only offering and there would be a need to offer a range of services including social media and e-commerce, gaming or any such combination such as ride hailing or food ordering apps that may combine to set up a much more attractive and combined digital only offering.

Existing banks are already targeting the online and digital space seeking to target new customer segments other than offering a digital range of services to existing customers. Some of the conventional players can become active investment partners in digital only banks as well.

Telcos with their extensive data sources and large customer bases are already very active in this space, including Easypaisa with Telenor and Jazz cash with Mobilink although their service offerings and objectives have been limited and not expanded upon toward a complete bank product offering.

It is therefore critical for the digital bank to be able to create an independent value proposition to reach enough customers for building a sustainable business. To differentiate from conventional bank digital products, a digital only bank must be able to develop unique capabilities so as to offer a differentiated service. As it is expected to be technology driven then it would be primarily a technology play with respect to user request processing, turnaround time management and AI-based tech driven risk management and credit evaluation capabilities.

Digital only banks must target potential profitability through aggressive customer onboarding and acquisition models early so as to ensure sustainability and not be driven by tech only value propositions focused only on customer reach and transaction-based milestones without effectively generating profits. Despite initial focus of scaling up like any tech venture the digital bank must have clearly defined path to profitability based on a realistic business model. Critical needs for ensuring a robust infrastructure with built in controls and security infrastructure not to expose the business and technology infrastructure to unwarranted risks.

The State Bank detailed regulations would help define a comprehensive framework towards enterprise level security and control infrastructure to grant any such future licensing approvals.

Ideally the success of this initiative would be dependent upon how well positioned any such offering can be made to enable a significant impact towards banking penetration, growth in online business and payments processing and ability to access new customers and achieve effective customer penetration through utilising technology and non-banking or non-conventional partner channels.

More importantly the success of digital banks and products need deep rooted reforms and enabling adjustments for which the government and SBP have been very progressive and already undertaken various steps which include:

• Recently unveiled national payment systems strategy, which introduces a new digital-focused framework to encourage the use of non-cash channels for payments in Pakistan.

• Working on a micropayment gateway that will democratise payments for all and lower the barrier for new entrants. The SBP aims to materialise the goals highlighted by the World Bank by the year 2025.

• Launch of the ‘Digital Pakistan’ initiative aimed at digitising the government’s core function for establishing a stabilised national economy. Under this project, the government aims to achieve five distinct goals that revolve around access and connectivity, digital infrastructure implementation, e-government, digital skills and literacy, and innovation and entrepreneurship.

• Launch of the new government-run instant digital payment system in a bid to boost financial inclusion and government revenue with new system “Raast” or “direct way”. Merchants, businesses, individuals, fintechs, and government entities will be able to send and receive near real-time payments through the internet, mobile phones and agents. Government payments, including salaries and pensions, will also be made through Raast, as well as payments for nationwide financial support programmes, such as the Benazir Income Support Programme, and the Ehsaas Emergency Cash Program already launched through the system in the pandemic support payments.

The writer is a staff member