The incumbent government has been facing multiple challenges that include economic revival, job creation, a reforms agenda in public sector entities and the energy sector, controlling the spread of COVID-19, governance and restoring the macroeconomic growth of the country.

The incumbent government has been facing multiple challenges that include economic revival, job creation, a reforms agenda in public sector entities and the energy sector, controlling the spread of COVID-19, governance and restoring the macroeconomic growth of the country.

During the first two years of this government, it has been widely criticised that the country’s debt has increased to alarming levels which has burdened the common man, increased socio-economic inequalities, and has further pushed the nation into debt. The government is of the view that this mess has been created by the previous regime.

A lot of blame game has been going on; in particular the previous government has been blamed for everything bad that has been done to the economy of Pakistan. However, this seems to fall within the purview of ‘political rhetoric’ rather than anything else. It may be noted that this sort of political rhetoric has previously affected Pakistan’s political stability as well as the investment climate of the country. Hence, the same must be abstained from as it only adds further confusion within an already complex and problem-laden system and does anything but resolving the complex economic issues we are faced with as a nation. The way forward should be a cohesive response by first identifying the main issues, and then resorting to resolve economic puzzles later. Once the issues have been identified, it should create an environment where it may be easier to resolve the problems.

With that being said, I will now move forward to analyse the overall debt situation of Pakistan.

Pakistan's debt has increased to unsustainable levels, and this has exposed the country to internal and external shocks. In addition to lack of reforms and inconsistent policies under the present regime, agreeing to the tough International Monetary Fund (IMF) conditionalities have negatively affected the economy. It needs to be assessed carefully and independently as to what has gone wrong during these two years. Why is the Pakistani economy passing through such a turbulent time, and what is the way forward to revive it?

High interests rates, devaluation of the rupee, electricity and gas prices, inflation, and other regulatory duties under the ongoing IMF programme have remained counter-productive, which has not only caused growth prospects to meltdown, but has also led to businesses struggling in a difficult situation. A reduction in real GDP growth of Pakistan to the tune of negative 0.38 percent was recorded this year. This is the lowest since 1951-52. Resultantly, socio-economic dynamics of our country have been damaged. It may be noted that this happened before the COVID-19 shock.

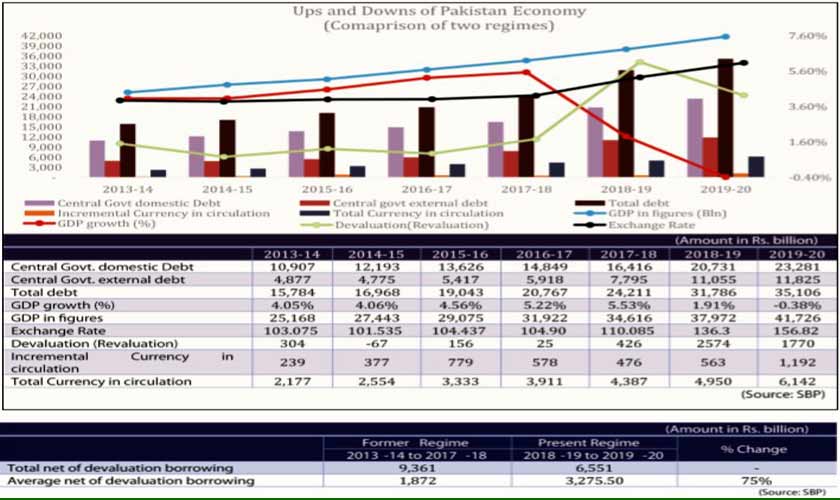

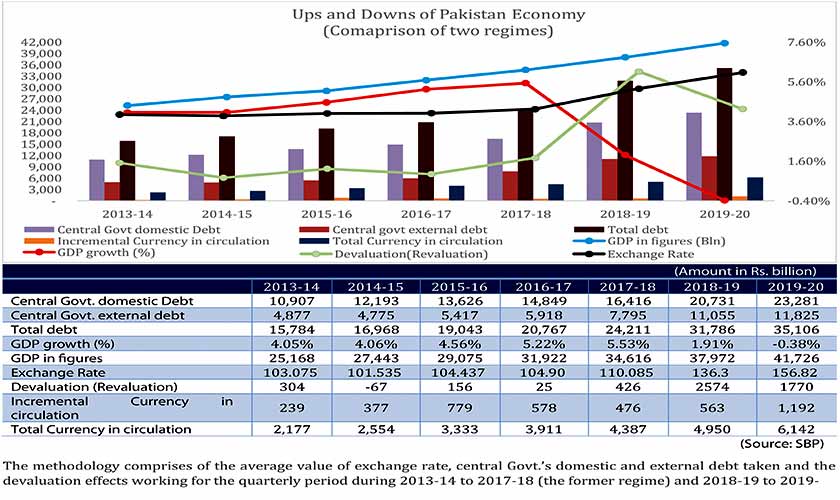

The methodology comprises of the average value of exchange rate, central government’s domestic and external debt taken and the devaluation effects working for the quarterly period during 2013-14 to 2017-18 (the former regime) and 2018-19 to 2019-20 (the present regime). Based on the above methodology, it is evident from the graph that Pakistan has had high GDP growth, a stable exchange rate and a lower average external and domestic debt of the central government per year during 2013-14 to 2017-18 as compared to 2018-19 to 2019-20.

Furthermore, the average devaluation effect on the Pakistani economy was lowest under the former regime as compared to the present regime. In addition to this, the average net of devaluation borrowing was also much lower during former regime as against the present regime. It is the harsh policies of the IMF which have pushed the country into a historic economic recession. Consequently, Pakistan’s GDP has dropped from a high growth of 5.53 percent in 2017-18 to negative 0.38 percent in 2019-20.

Domestic debt, external debt and the devaluation effect are three critical factors to determine the performance of the two regimes. The comparison of the average external and domestic debt per year during the two regimes can be seen in the chart above

Under the previous regime, the gross average domestic debt per year remained at Rs1,379 billion mainly because of a low interest rate environment. As a result, due to low interest rates and higher tax revenue collection, fiscal deficit dropped to 6.5 percent of GDP by the end of FY2018 as compared to 8.2 percent of GDP in FY2013. Whereas, under the present regime, gross average domestic debt per year has appreciated by Rs3,432 billion, which is 149 percent higher than the previous regime mainly due to a high policy rate which grew from 7.50 percent as of July 2018 to 13.25 percent till July 2019. Hence, in addition to high interest rates, higher financing needs and low tax revenues, the fiscal deficit has remained at alarming levels of 8.9 percent of GDP in 2018-19 and 8.10 percent of GDP in 2019-20.

Moreover, during the previous regime, the gross average central external debt per year grew by Rs661 billion during 2013-14 to 2017-18 mainly due to the concessional long-term loans utilised in structural reforms in the energy sector, infrastructure, CPEC projects, SMEs, taxation, and trade facilitation which had also enhanced the debt repayment capacity. Whereas, under the present regime, the gross average central external debt has grown by Rs2,015 billion or 204 percent higher versus the previous regime mainly due to a massive rupee devaluation by 23.82 percent in 2018-19 and 14.93 percent in 2019-20. Under the present regime, the total central government domestic and external debt grew by Rs10,894 billion or 45 percent from Rs24,211 billion (FY2018) to Rs35,106 billion (FY2020). Whereas, during the previous regime, the central government’s external and domestic debt grew by Rs10,204 billion or 72.84 percent from Rs 14,007 billion (FY2013) to Rs24,211 billion (FY2018). However, on an average basis, the gross total central domestic and external debt grew by 166 percent Rs5,447 billion in the present regime as compared to Rs2,040 billion during the previous regime.

Overall, Pakistan’s average exchange rate remained stable from 2013-14 to 2016-17. However, it dropped by 14 percent from Rs96.95/dollar during 2012-13 to Rs110.64/dollar during 2017-18, which had caused devaluation effects of Rs844 billion to the economy (average Rs.69 billion). Under the present regime, the country’s average exchange rate has deteriorated by 42 percent from Rs110.64/dollar in 2017-18 to Rs156.82/dollar in 2019-20 which has triggered massive devaluation effects of Rs4,344 billion for the economy (average Rs2,172 billion). The average net of devaluation borrowing under the previous regime stood at Rs1,872 billion during 2013-14 to 2017-18, which has appreciated by 75 percent to Rs3,275 billion under the present regime. Whereas, the total net off devaluation borrowing during the present regime of two years stood at Rs6,551 billion as compared to Rs9,361 billion during the previous regime of 5 years. In terms of average incremental stock of currency in circulation per year, under present regime it has grown by Rs878 billion versus Rs490 billion during the last regime.

Pakistan’s current account deficit dropped by 78 percent to $2.96 billion during FY20 from $13.43 billion during FY19 billion last year. In order to achieve macroeconomic stability, the country was required to focus on an export-led growth, capital goods and essential raw material imports which were cut down that slowed down our GDP growth. Although exports were relatively lower under the previous regime, it might be pertinent to mention here that most of CPEC and power-related imports were recorded in 2016-17 and 2017-18, which were essential for consistent growth of CPEC projects that country had to achieve for macroeconomic sustainability and the changing security paradigm of the region. Therefore, higher CPEC related and specialised imports had escalated the current account deficit to around $19 billion in 2017-18.

Due to the economic recession, the FBR missed its tax revenue collection target by a wide margin of Rs1,675 billion during 2019-20, which has exhausted fiscal space of the country. The gravity of the situation can be understood from the fact that the country’s “interest servicing” to FBR’s tax revenue grew significantly from 39 percent in 2017-18 to around 72 percent in 2019-20, based on the budgeted figures. This indicates that interest payments grew at an alarming pace, while tax revenues remained stagnant. Pakistan’s low tax revenue collection and high fiscal deficit is a real impediment to achieve sustainable growth.

Going forward, Pakistan must renegotiate its terms with the IMF in order to reduce uncertainty and vulnerability within the economy. The policy rate should be further slashed down to 3-4 percent to stimulate GDP growth and revive demand. Tax reforms should be implemented as per the TRC report submitted in January 2016. In addition to this, the government should reduce dollar parity to Rs140 through central bank intervention, and give direct subsidy to the exporters in rupees to compensate alignment of rupee dollar parity. Printing of notes should only be used for the economic development of the country, and governance issues should be addressed to control inflation.

The writer is a tax expert