The elimination of ‘captive power’ in Pakistan’s gas sector, set as a structural IMF benchmark for January 2025, could deeply impact the industrial sector.

The elimination of ‘captive power’ in Pakistan’s gas sector, set as a structural IMF benchmark for January 2025, could deeply impact the industrial sector.

In-house power generation, critical for many industries and upheld by the Supreme Court, was misclassified under a ‘captive’ gas tariff in 2019. This shift aims to reallocate gas to ‘more efficient’ RLNG-based Government Power Plants (GPPs), but recent analysis from Socioeconomic Insights and Analytics warns this may trigger deindustrialisation, with potential export losses of $3 billion and over three million job cuts.

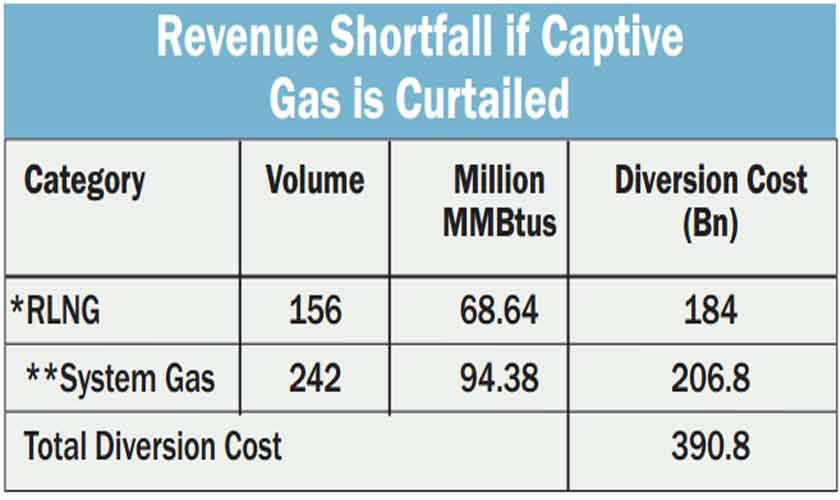

The policy also threatens goals such as expanding renewable energy, developing a distributed grid, and advancing cleaner cogeneration technologies. Furthermore, removing bulk RLNG consumers like Captive Power Plants (CPPs) risks a Rs390.8 billion revenue shortfall for Sui companies, endangering the cross-subsidy that supports residential gas rates -- an action with social and political implications. Without a reallocation plan, ‘Take or Pay’ penalties on LNG cargoes may occur, which could be passed on to RLNG consumers, potentially destabilising state-owned entities within the Petroleum Division.

CPPs currently consume 176 mmcfd of RLNG, with no other sector positioned to absorb this demand, risking increased Unaccounted-for Gas (UFG) rates, reduced revenue, and restricted improvements to the gas infrastructure. Meanwhile, Pakistan’s rapid power generation expansion has outpaced its Transmission and Distribution (T&D) network, leading to frequent outages, high line losses, and rising costs, contributing to a circular debt of Rs2.636 trillion.

Transitioning industries from self-generation to the national grid is complicated by infrastructure gaps, high costs, and grid unreliability. Industries have invested heavily in gas-fired power facilities; removing gas from these setups would result in sunk costs of Rs128 billion in the textile sector alone. The switch to an unreliable grid would demand substantial time and financial investments in new infrastructure.

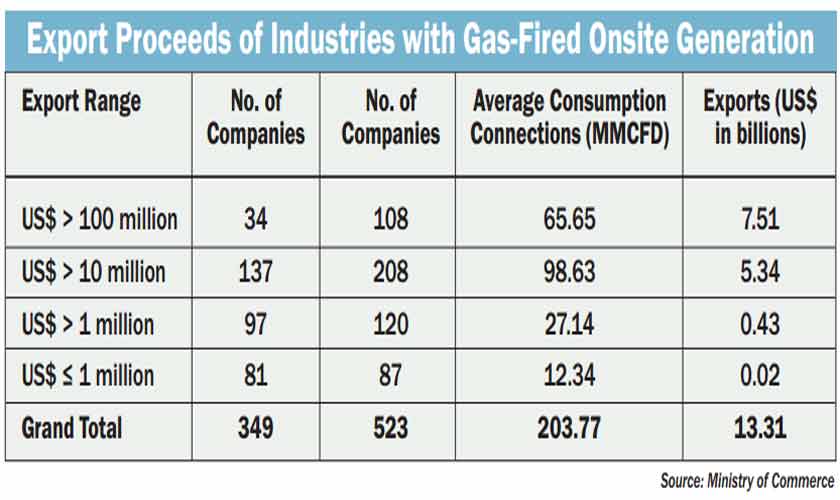

Self-generation plays a crucial role in supporting exports, and regulatory changes to gas supply should carefully consider potential economic impacts. Ministry of Commerce data shows that 34 top exporters, consuming 65.65 mmcfd of gas at nearly double the Ogra-prescribed rate, generated $7.51 billion in exports in FY 2022, with 137 more firms contributing $5.33 billion. This $13.31 billion total emphasises the sector's critical role in the national economy.

Currently, there are 387 captive power plants (CPPs) on the SNGPL network, consuming an average of 157 mmcfd -- split into 54 mmcfd of System Gas and 103 mmcfd of RLNG. These plants receive a 25:75 blend of system gas and RLNG at a blended tariff of Rs3,446 per MMBtu (as of October 2024), while Government Power Plants (GPPs) benefit from a lower tariff of Rs3,352 per MMBtu. Similarly, SSGC operates 752 CPPs, consuming 180 mmcfd on average, with 130 mmcfd from System Gas and 50 mmcfd from RLNG. The blend ratio shifts seasonally: 60:40 in the winter and 80:20 in the summer.

According to Ogra’s SNGPL Revenue Requirement decision (May 20, 2024), the RLNG diversion cost is Rs3,400 per MMBtu ($12.19 per MMBtu), while diverting system gas from captive power to the power sector costs Rs1,950 per MMBtu. A cutoff in gas supply to captive consumers would lead to a substantial revenue shortfall of Rs390.8 billion for both Sui companies.

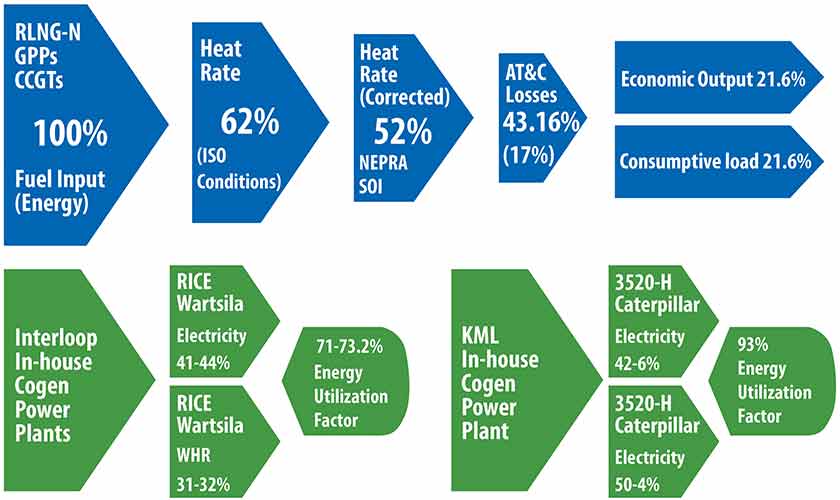

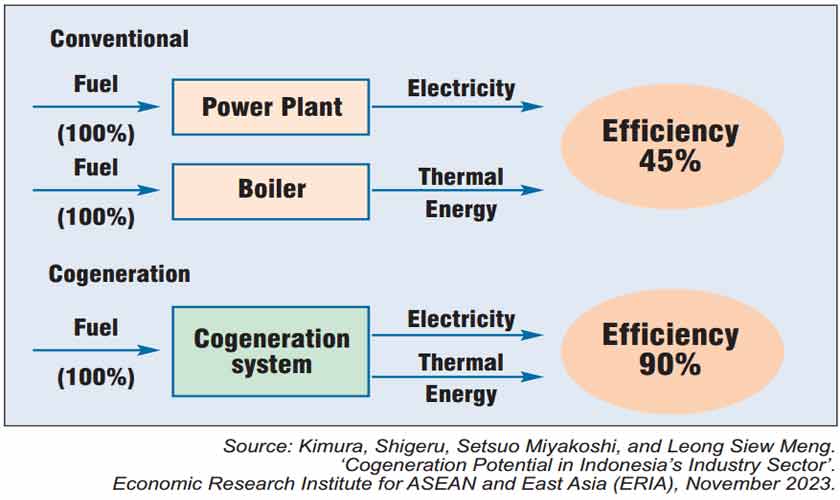

The elimination of captive power assumes that redirecting gas to RLNG Government Power Plants (GPPs) will optimise resource use, based on their theoretical 62 per cent efficiency. However, in practice, GPPs operate at around 52-53 per cent efficiency under real-world conditions, dropping further to 43.16 per cent when accounting for grid transmission losses, according to Nepra data. In contrast, onsite generation facilities like Combined Heat and Power (CHP) systems achieve up to 90 per cent efficiency, with minimal distribution losses.

A balanced energy strategy that integrates both grid-based and localised power generation is essential to preserve Pakistan’s industrial competitiveness, promote sustainable economic growth, and ensure energy security. Rather than cutting off their gas supply, industrial in-house power generation facilities should be reclassified as industrial processes and treated accordingly

RLNG GPPs are costlier and often operate below capacity, as cheaper baseload options like coal and nuclear are prioritised. This curtailment and non-steady-state operation reduce efficiency, increase fuel consumption, and accelerate equipment wear. Moreover, RLNG diverted to residential consumers, often subsidised, is a key contributor to the sector’s circular debt, now at Rs2.7 trillion.

Gas turbines also suffer from frequency instability when synchronised with the grid, further reducing thermal efficiency. Meanwhile, approximately 8,000MW of low-efficiency, oil-based IPPs from the 1994 and 2002 policies continue to operate without energy efficiency audits. Using single-cycle technology, these IPPs rely on costly Furnace Oil (FO) and High-Speed Diesel (HSD), passing fuel costs onto consumers and inflating tariffs.

This transition away from captive power risks destabilizing the gas sector financially, encourages underutilised coal-based generation, and undermines distributed energy benefits. Distributed generation through CHP plants, endorsed by the World Bank and IMF, improves grid resilience, reduces transmission losses, and supports sustainable, decentralized power. The IMF’s 2010 Poverty Reduction Strategy Paper for Pakistan highlighted the potential of cogeneration in improving energy security and efficiency, particularly in industries like sugar, to generate over 3,000MW from waste heat.

Single-cycle plants achieve up to 45 per cent efficiency, while CHP plants can reach 90 per cent by generating both electricity and heat from a single fuel source. CHP systems reduce waste by using captured heat for industrial processes, delivering two energy outputs from a single gas molecule, thus outperforming traditional power plants in efficiency and sustainability.

In the textile sector, which relies heavily on stable and cost-effective energy solutions, Combined Heat and Power (CHP) systems provide a substantial competitive edge. These systems not only deliver consistent and efficient power directly at the point of use but also lower operational energy costs. By generating power on-site, CHP systems greatly reduce dependency on lower-quality grid electricity, which is especially beneficial given the high thermal energy needs of textile processes such as dyeing, fabric finishing, and spinning. This efficient energy use not only strengthens the economic stability of textile operations but also enhances their global competitiveness by bolstering their sustainability profiles and aligning with international environmental standards.

The proposed disconnection of gas supply to captive power plants (CPPs), which are effectively on-site industrial generation facilities, represents a fundamentally flawed policy that threatens economic stability and social welfare. It overlooks the high operational efficiency and superior energy utilization of on-site generation, particularly Cogeneration systems, which achieve up to 90 per cent energy efficiency. Disrupting gas supply to in-house power generation could seriously destabilise key industries like textiles, which depend on steady, affordable energy to sustain production, export competitiveness, and jobs for millions. Such a move risks not only deepening the circular debt crisis and lowering export earnings but also broader socio-economic consequences, including increased unemployment and economic contraction.

Policymakers must urgently reevaluate this approach, recognising the vital role of on-site power generation in supporting industrial growth, energy resilience, and economic diversification. A balanced energy strategy that integrates both grid-based and localised power generation is essential to preserve Pakistan’s industrial competitiveness, promote sustainable economic growth, and ensure energy security. Rather than cutting off their gas supply, industrial in-house power generation facilities should be reclassified as industrial processes and treated accordingly to reflect their actual usage accurately.

It is critical for decision-makers to adopt a holistic, data-driven strategy that maximises efficiency, minimises risks, and supports the long-term development of the industry and economy.

Shahid Sattar is a former energy member of the Planning Commission, and currently working as secretary-general of the All Pakistan Textile Mills Association (APTMA).

Absar Ali is a senior economist at APTMA.

Asim Riaz is an energy adviser at APTMA.