Generally, Pakistan turns to the International Monetary Fund (IMF) when the country faces a current account deficit (CAD). Due to the adoption of IMF policies, Pakistan then has to deal with a fiscal deficit too.

Generally, Pakistan turns to the International Monetary Fund (IMF) when the country faces a current account deficit (CAD). Due to the adoption of IMF policies, Pakistan then has to deal with a fiscal deficit too.

Typically, the IMF’s strategies provide short-term stabilization, but Pakistan has often faced significant challenges under these programmes. The IMF programme from 2013 to 2016 was the only successfully completed programme of the last two decades. Following that, the deterioration of economic indicators and a high CAD in during FY2017-18 necessitated Pakistan to pursue another IMF programme in 2019. This later programme had detrimental impacts on Pakistan’s economy due to specific policy measures. Notably, the focus on attracting hot money and raising the policy rate to double digits imposed a considerable strain on the economic landscape and exacerbated financial instability.

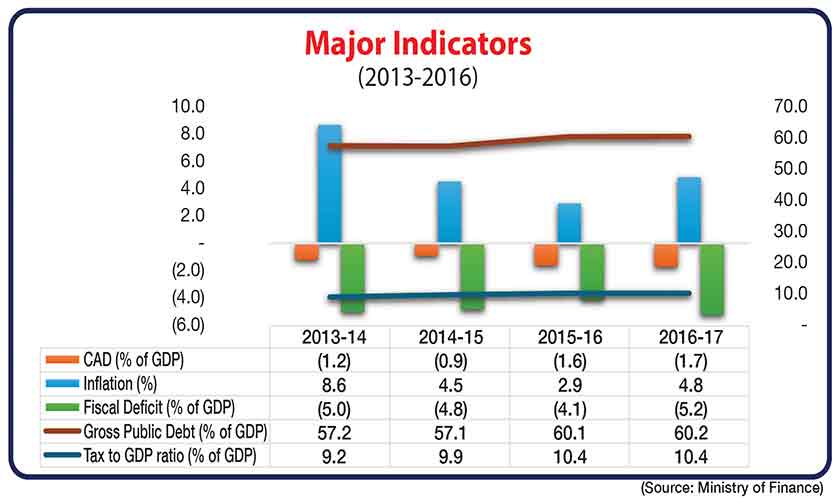

Table 1 illustrates the major macroeconomic performance under the IMF programme.

In FY18, Pakistan faced a significant CAD amounting to 5.4 per cent of GDP. Fiscal deficit was also rising, increasing from 5.2 per cent in FY17 to 5.8 per cent in FY18. Due to this economic uncertainty, Pakistan entered into an IMF programme in 2019. Subsequently, currency devaluation began, and inflation rose to double digits in the next fiscal years. This IMF programme has not been favourable, as Pakistan is required to adhere to the IMF’s stringent policies.

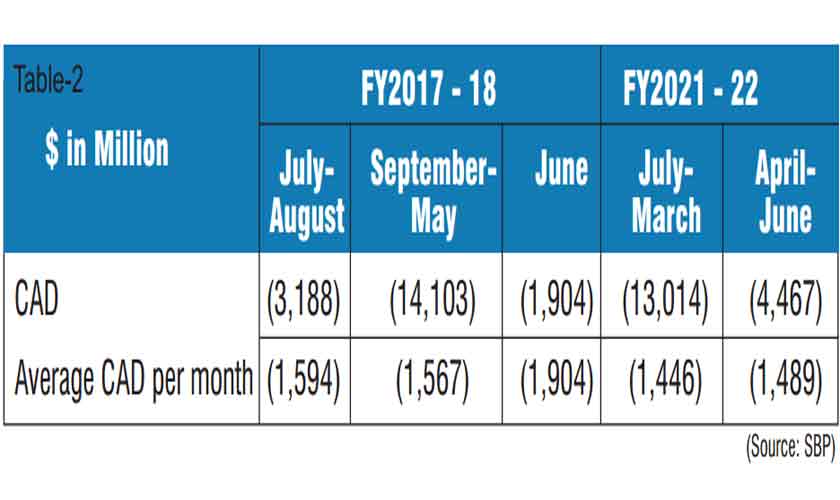

During 2017-18, the country had three economic teams. Table 2 illustrates the periods where CAD surged to a record level.

During FY22, the economic situation in Pakistan became very fragile due to significant external sector imbalances and high import bills, necessitating funds to manage the deficit. During this period, Pakistan faced a high twin deficit, where CAD of 4.7 per cent of GDP, and the overall fiscal deficit reached 7.9 per cent of GDP.

As a result, Pakistan badly needed to resume the suspended 7th and 8th reviews of the Extended Fund Facility programme and implement the IMF’s tough policies to secure it. Due to the uncertainty, the country experienced record inflation and currency devaluation in FY23. The policy rate was raised to 22 per cent in an attempt to control inflation, yet it failed to do so, with inflation surpassing 30 per cent on a year-on-year basis.

Moving forward, FY24 is relatively a stable year, primarily because the CAD is well below the $1 billion mark, clocking in at $681 million for the July-June period. This stability is not due to the IMF’s recommendations, as the IMF predicted the CAD would be around $6 billion. However, if Pakistan had not imported $1.032 billion worth of wheat in FY24, the country would have been in a surplus position.

Additionally, in recent statements, the honourable finance minister and other high-ranking government officials have asserted that Pakistan’s economy is on the path to stability. They have emphasized that the country is geared up for a new IMF programme, which is expected to further consolidate this stability. This narrative comes at a crucial time, as Pakistan seeks to address longstanding economic challenges and foster sustainable growth.

If stabilization is truly present, then why is the State Bank of Pakistan buying dollars at a higher rate, which creates inflationary pressure in the economy? A significant aspect of Pakistan’s economic strategy involves the Home-Grown Plan, which is set to be a cornerstone of FY25 if implemented.

The Home-Grown Plan includes several key measures like: (a) reducing the policy rate; (b) keeping import levels reasonable; (c) bringing currency parity to the real value of Rs233-235 over one dollar; (d) compensating exporters in local currency; (e) providing incentives for remittances in local currency; (f) implementing tax reforms as per the Reforms and Resource Mobilization Commission (RRMC) report; and (g) promoting export-led growth through the Special Investment Facilitation Program’s (SIFC) Green Pakistan initiatives.

The outcomes of this plan are projected to be substantial. GDP growth is expected to reach 4.0 per cent; the fiscal deficit will be at 2.4 per cent of GDP; and the CAD will be around 0.5 per cent of GDP. Additionally, the total import bill will be limited to $54 billion for goods and $8.62 billion for services. Remittances are expected to reach $33 billion, and exports will surge to $43 billion, with $35 billion in goods and $8 billion in services. Additionally, the FBR tax collection will be Rs13 trillion in FY25.

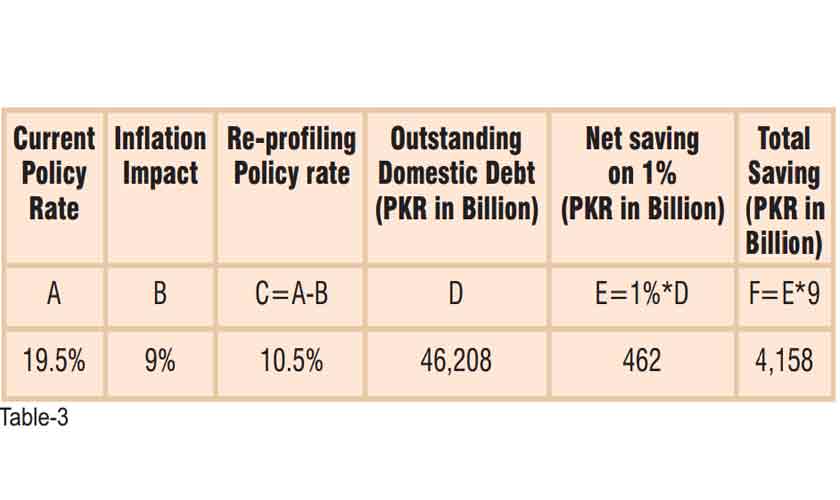

Maintaining the currency’s value in line with its true market value is essential for balanced trade and investment. However, concerns exist about the currency’s true value not being accurately reflected against the US dollar. According to the latest FY24 data, the true value of the currency at the end of FY24 is Rs233/USD, with a required REER rate change of 13.86. A 2.0 per cent inflation pass-through occurs with every 10-rupee devaluation against the dollar. If the USD/PKR declines by 45 rupees, inflation may decrease by 9.0 per cent, leading to a potential 9.0 per cent decline in the interest rate, saving Rs4158 billion in fiscal space. (Table-3)

If the Home-Grown Plan is executed effectively in FY25, it could lead to a substantial improvement in the country’s economic standing, potentially resulting in a current account surplus. Such a shift would signify a major step towards economic self-sufficiency and stability, aligning with the broader goals outlined by the government’s economic policymakers. If the Home-Grown Plan is not executed and the IMF’s policies are followed instead, the result would be inflationary pressure of more than 20 per cent projected figure. A research house, AUGAF, has already cited Bloomberg’s prediction that Pakistan’s currency will devalue to Rs350/USD by the end of FY25, adding another 14 per cent of inflationary pressure to the already struggling economy.

Currently, the IMF states that Pakistan has a gross repayment amount of $21 billion. However, the net repayment amount is $7 billion. In this case, we need a moratorium from Saudi Arabia, China, UAE, and Qatar. Therefore, Pakistan requires $7 billion for loan repayment. With exports at $43 billion (including services), remittances at $33 billion, and imports at $62 billion (including services), we can save $14 billion and use $7 billion for repayment. This leaves us able to repay the moratorium amount of $7 billion as well.

If we achieve the moratorium, why do we need the IMF? The IMF provides more loans, but if reserves remain constant and the SBP acquires $7 billion, there is no need for the IMF. Pakistan needs to revisit its industrial policies, attract dollar-based investments to boost dollar-based exports, and ensure FDI aligns with green initiatives through the SIFC. Additionally, the privatization process should be transparent, with proceeds used for debt repayment.

The writer is a former minister of state, former chairman of the RRMC, former president of the Institute of Chartered Accountants, and the current vice-president of the South Asian Federation of Accountants (SAFA).