MINERALS

Mineral sector offers enormous potential for playing a vital role in the economic development, but, sadly, it has been neglected by the successive governments. National Mineral Policy 2013, which was updated and revised in March 2014, has failed to achieve the targeted results - to give desired impetus to the mineral sector and to attract investors.

Likewise, Khyber Pakhtunkhwa’s first Mineral Policy announced in July 2014 has not been implemented effectively and forcefully as yet, since the mineral sector’s legislative and fiscal regime is domain of the federal government, although provinces are the major stakeholders.

Likewise, Khyber Pakhtunkhwa’s first Mineral Policy announced in July 2014 has not been implemented effectively and forcefully as yet, since the mineral sector’s legislative and fiscal regime is domain of the federal government, although provinces are the major stakeholders.

A case in point is the need for development of phosphate rock, an important non-metallic mineral. Rock phosphate, a major source of phosphorus, is an essential element for plant and animal nutrition. It is thus used as an organic fertiliser in its raw form, and is the raw material for production of processed phosphate (or phosphatic) fertilisers, phosphoric acid and other industrial chemicals and animal-feed. Extensive geological surveys have proved potential deposits of 26 million tons of phosphate rock of all grades, which is sufficient to meet the country’s total requirement of phosphate fertilisers for nearly 30 years.

Also, it is estimated that inferred reserves of phosphate rock could be in the range of 200 million tons, but further extensive geological surveys and investigations are required. Though vast resources of phosphate rock mineral offer great potential for economic extraction, exploitation and utilisation, its physical extraction remains almost static at 400,000 tons per year, and obsolete opencast manual methods are still employed for mining.

Globally, there exist more than 300 billion tons resources of phosphate, including over 67 billion ton mineable reserves, in more than 23 countries. Morocco has more than half of the world’s total phosphate deposits where it is called “white gold”, while US and China have the other major global shares. Currently, total global production is 200 million tons a year.

About 85 percent of total mined phosphate is used for fertilisers, five percent for animal-feed, a small percentage for feed additives, and remainder as chemical compounds for industrial and commercial purposes, such as detergents. Phosphate rock, in the form of unprocessed ore and processed concentrate, is a finite mineral indispensable for fertiliser production.

Phosphate fertilisers are gaining popularity in Pakistan sharply year-by-year. One of the key elements to increasing agricultural yield is better provision of fertilisers and seeds. Inadequate use of fertilisers and imbalance in the ratio of nutrients are major factors affecting the crop yield. Major phosphorus deficiencies exist in the soil due to under-fertilisation with phosphorus-containing fertilisers. To promote use of phosphate fertilisers, the government had announced in October 2015 a one-time subsidy of Rs20 billion to farmers through local fertiliser producers and commercial importers of these types of fertilisers.

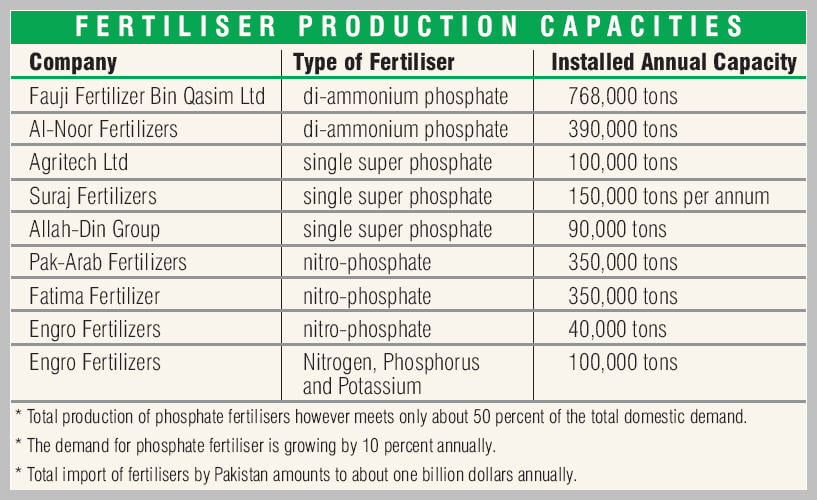

Currently, Pakistan has an installed capacity of three million tons for production of all types of phosphate fertilisers, though it is being operated at about 40 percent of installed capacity due to various factors. A variety of these fertilisers include di-ammonium phosphate (DAP), single super phosphate (SSP), nitro-phosphate (NP) and mono-ammonium phosphate (MAP). Fauji Fertilizer Bin Qasim Ltd has an installed annual capacity of producing 768,000 tons DAP, whereas Al-Noor Fertilizers has DAP production capacity of 390,000 tons annually. Fertiliser SSP is produced by Agritech Ltd (former Hazara Phosphate Fertilizers Ltd) having capacity 100,000 tons per annum. Suraj Fertilizers have installed capacity 150,000 tons per annum, and Allah-Din Group (former Lyallpur Chemicals and Fertilizers Ltd) has a capacity of producing 90,000 tons of SSP fertiliser annually.

Cumulative production capacity for NP fertilizer in Pakistan is at the level of 740,000 tons per year, major players being Pak-Arab Fertilizers (350,000 tons), Fatima Fertilizer (350,000 tons) and Engro Fertilizers (40,000 tons). Engro Fertilizers’ annual installed capacity for NPK fertiliser (Nitrogen, Phosphorus and Potassium) production is 100,000 tons. The total production of phosphate fertilisers however meets only about 50 percent of the total domestic demand, which is growing by about 10 percent annually. The supply-demand gap is thus filled through imports. Total import of fertilisers by Pakistan amounts to about one billion dollars annually, of which phosphate fertilisers constitute significant share. In 2008, phosphate fertilisers valuing $24.5 million were imported.

Even to meet the requirements of the domestic industrial units fully, the feedstock is being imported, instead of optimal extraction and maximum use of indigenous phosphate rock. Due to inadequate and irregular supply of local phosphate rock, the fertiliser units resort to large-scale imports, primarily from Jordan and Morocco.

Even to meet the requirements of the domestic industrial units fully, the feedstock is being imported, instead of optimal extraction and maximum use of indigenous phosphate rock. Due to inadequate and irregular supply of local phosphate rock, the fertiliser units resort to large-scale imports, primarily from Jordan and Morocco.

There exist two major phosphate rock types, namely dolomite ore, containing low to medium phosphorus pentoxide (P2 O5) and siliceous ore containing medium to high P2 O5. The proven reserves, commonly known as Hazara phosphates, are estimated to be 14 million tons and 12 million tons of the respective ores. Based on a series of comprehensive studies on the phosphate rock deposits and the use of mineral, a number of sources have been identified, though main beds are located near the villages Kakul-Mirpur and Lagarban-Tarnawai and Serban Hill areas in Hazara Division. These are commercially exploitable deposits.

There are some 750,000 tons of phosphate rock of acceptable quality available at Kakul alone. This grade could be used, blended with imported high quality phosphate rock, to produce other phosphate fertilisers. Tarnawai deposits, of about two million tons, are of better grade and quality averaging 28.5 percent P2 O5. The quality and quantity of Tarnawai reserves thus meet the requirement of the fertiliser industry and could absorb the cost of developing mines over the total tonnage eventually extracted.

Phosphate rock mining remains focused at Kakul, district Abbottabad, whereas Tarnawai deposit has recently been developed. An integrated Kakul phosphate-mining project was planned in 1985, basically to feed the SSP fertiliser-producing plant located in Hazara, which was designed to process local phosphate rock of Kakul and Tarnawai origins, to produce 90,000 tons of granulated SSP per annum. The project did not materialise.

Responding to the economic and social needs, the development of national phosphate resources and optimising its use for production of fertilisers should be a priority objective of the government. In view of the minerals’ importance in achieving industrialisation, import substitution and export promotion, the policy needs to address the issues hampering its large-scale development.

The writer is ex-chairman of State Engineering Corporation